A Complete Step-by-Step Guide

Buying a home is one of the biggest financial decisions most people will ever make. Scotland has a unique property buying system that differs from the rest of the United Kingdom, particularly England and Wales. Understanding how the Scottish property market works can help buyers avoid surprises and make informed decisions.

This guide explains the requirements, costs, documents needed, and the entire process of buying a house in Scotland.

.

Why Buy Property in Scotland?

Scotland offers a diverse range of housing options, from city apartments in Edinburgh and Glasgow to rural cottages in the Highlands and coastal homes in Moray and Aberdeenshire. Property prices are often lower than in many parts of southern England, making Scotland attractive for first-time buyers, families, retirees, and investors.

.

Who Can Buy a House in Scotland?

There are very few restrictions on who can purchase residential property in Scotland.

You can buy a property if you are:

- A UK citizen

- A resident of Scotland

- A foreign national

- An expatriate living abroad

- An investor purchasing a second home

The main requirement is proving that you can legally fund the purchase and, if required, obtain a mortgage.

.

Step 1: Assess Your Finances

Before viewing properties, determine how much you can afford.

Consider:

- Your available deposit

- Mortgage affordability

- Monthly income and expenses

- Existing debts and financial commitments

- Additional purchase costs

Most lenders require a deposit of between 5% and 20% of the property’s purchase price, although larger deposits usually provide access to better mortgage rates.

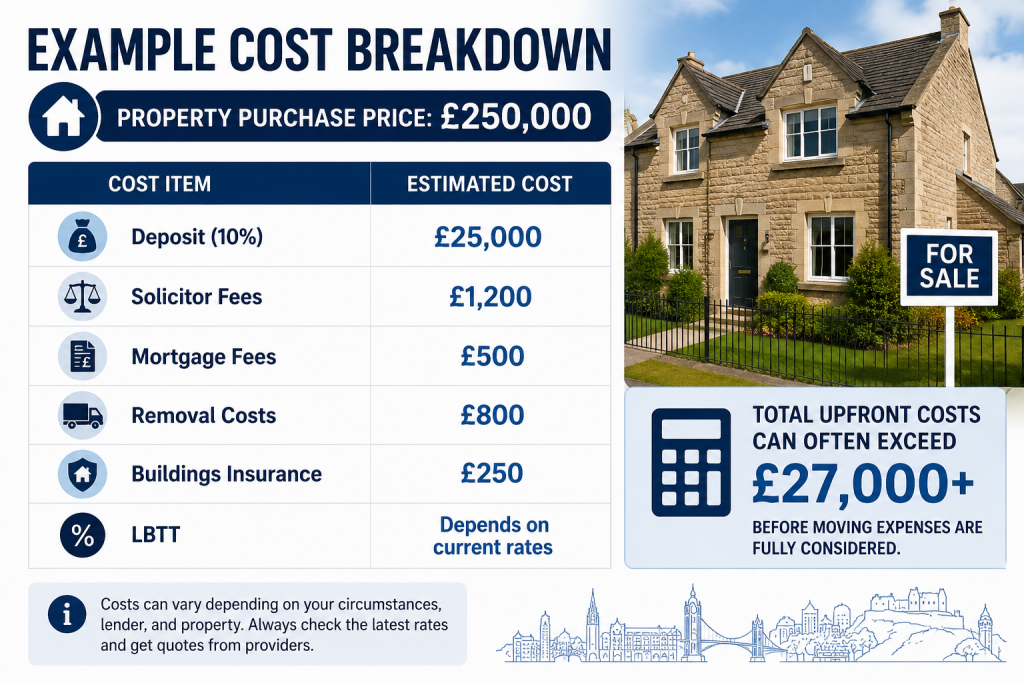

Example

Property price: £250,000

- 10% deposit: £25,000

- Mortgage required: £225,000

.

Step 2: Obtain a Mortgage Agreement in Principle

An Agreement in Principle (AIP), sometimes called a Mortgage in Principle, is a statement from a lender indicating how much they may be willing to lend.

Although not legally required, most estate agents and sellers prefer buyers who already have mortgage approval in principle.

Documents typically required include:

- Passport or driving licence

- Proof of address

- Recent payslips

- Bank statements

- Tax returns for self-employed applicants

- Proof of deposit funds

.

Step 3: Find a Property

Properties in Scotland are commonly marketed through:

- Estate agents

- Property websites

- Solicitors’ property centres

- New-build developers

Most properties are advertised with an “Offers Over” price.

This means:

- The advertised figure is usually a guide price.

- Popular properties may sell for more than the listed amount.

- Buyers submit formal offers through their solicitor.

.

Step 4: Review the Home Report

One unique feature of the Scottish system is the Home Report.

Most residential properties for sale must provide a Home Report before being marketed.

The report contains:

Single Survey

A professional assessment of the property’s condition and value.

Energy Report

The property’s Energy Performance Certificate (EPC).

Property Questionnaire

Information provided by the seller regarding:

- Council tax band

- Alterations and extensions

- Parking arrangements

- Utility information

- Local authority matters

Always read the Home Report carefully before making an offer.

.

Step 5: Appoint a Solicitor

In Scotland, a solicitor plays a crucial role in the property purchase process.

Your solicitor will:

- Submit offers

- Conduct legal checks

- Review contracts

- Handle property transfer

- Register ownership

- Transfer purchase funds

Legal fees typically range from £800 to £2,000 depending on the complexity of the transaction and property value.

.

Step 6: Make an Offer

Once you find a suitable property, your solicitor submits a formal offer on your behalf.

The offer usually includes:

- Purchase price

- Proposed completion date

- Conditions of purchase

- Items included in the sale

If multiple buyers are interested, the seller may set a “closing date.”

At a closing date:

- All interested parties submit offers.

- The seller chooses the preferred offer.

- The highest offer is not always accepted.

.

Step 7: Concluding Missives

Missives are a series of legal letters exchanged between solicitors.

These letters contain:

- Purchase conditions

- Agreed price

- Completion arrangements

Once missives are concluded:

- The contract becomes legally binding.

- Neither party can withdraw without significant legal consequences.

This is generally much earlier in the process than in England and Wales, providing greater certainty for buyers and sellers.

.

Step 8: Final Mortgage Approval

Your lender will complete final checks before releasing funds.

You may need to provide:

- Updated bank statements

- Additional proof of income

- Proof of deposit source

- Identification documents

The lender will issue a formal mortgage offer once approved.

.

Step 9: Settlement Day

Settlement, often called completion day, is when ownership officially changes.

On this day:

- Mortgage funds are transferred.

- The purchase balance is paid.

- Ownership transfers to the buyer.

- Keys are released.

You can then move into your new home.

.

Step 10: Property Registration

Following settlement, your solicitor will:

- Register ownership with Registers of Scotland.

- Pay any applicable taxes.

- Complete final legal formalities.

Once registration is complete, you become the officially recorded owner of the property.

.

What Documents Are Required?

Personal Identification

- Passport

- Driving licence

- Residence permit (if applicable)

Proof of Address

- Utility bill

- Council tax statement

- Bank statement

Financial Documents

- Payslips

- Employment contract

- P60

- Tax returns (for self-employed buyers)

- Bank statements

Deposit Evidence

- Savings account statements

- Gift letters (if family members contribute)

- Evidence of investment withdrawals

Mortgage Documentation

- Agreement in Principle

- Mortgage application paperwork

- Formal mortgage offer

.

What Taxes Must Be Paid?

Land and Buildings Transaction Tax (LBTT)

Scotland uses LBTT instead of Stamp Duty.

The amount payable depends on:

- Purchase price

- Whether the property is your main residence

- Whether it is an additional property

Rates are subject to change, so buyers should check current Scottish Government guidance before purchasing.

Additional Dwelling Supplement (ADS)

Buyers purchasing:

- Second homes

- Holiday homes

- Buy-to-let properties

may have to pay Additional Dwelling Supplement on top of LBTT.

.

Typical Costs of Buying a House in Scotland

Deposit

Usually 5% to 20% of purchase price.

Solicitor Fees

Typically:

£800 to £2,000

Mortgage Fees

Potential costs include:

- Arrangement fees

- Valuation fees

- Broker fees

Removal Costs

Typically:

£300 to £2,500 depending on distance and volume.

Buildings Insurance

Required by most mortgage lenders before completion.

LBTT and ADS

Where applicable.

.

Example Cost Breakdown

.

First-Time Buyer Tips

- Obtain a Mortgage Agreement in Principle before viewing properties.

- Carefully review the Home Report.

- Budget for legal fees and taxes.

- Avoid stretching affordability to the maximum offered by lenders.

- Compare mortgage products from several lenders.

- Use an experienced Scottish property solicitor.

.

Advantages of the Scottish Buying Process

The Scottish system offers several benefits:

- Greater transparency through Home Reports.

- Earlier legal commitment.

- Reduced risk of transactions collapsing.

- Faster completion times.

- Clear legal procedures.

Final Thoughts

Buying a house in Scotland is generally considered a straightforward and well-regulated process. While the legal system differs from other parts of the UK, the use of Home Reports and early legal commitment provides greater certainty for both buyers and sellers.

Careful financial planning, obtaining mortgage approval in advance, and working with an experienced solicitor will help ensure a smooth and successful property purchase. Whether you are buying your first home, relocating to Scotland, or investing in property, understanding the process is the first step towards making your purchase with confidence.